Reuters and EBS built the institutional FX data backbone in the 1990s. Bloomberg put a terminal on every desk that could afford one. TraderMade was on those same desks — we've provided FX charting and analysis to the interbank market since 1984, and for decades our charts were the ones that many FX dealers and analysts at the major banks kept open through the trading day. We still provide charting services to banks today.

So this comparison comes from a firm that knows this infrastructure from the inside. We've run institutional FX infrastructure alongside these firms for four decades, and in 2017, we saw where data consumption was heading and moved early: extending the business into API-first, data-first delivery, built for the way modern systems consume market data.

The systems consuming FX data today are trading platforms, brokerages, quant engines, payment apps and fintech products, built by engineering teams who expect data to arrive through modern APIs, in days not weeks, under contracts that don't require weeks of negotiations.

This is where the comparison actually gets decided. Not on whether the established providers have good data, they do. On whether your workload still needs the architecture, the onboarding process, and the cost structure that come attached to it.

For most teams building products on FX data today, we'd argue it doesn't. Here's the detailed case, with the tests to verify every claim yourself.

The Rate Quality Question

Enterprise price tags carry an implicit promise: that the rates behind them are somehow better. Before paying for that promise, it's worth asking what "better" actually means at the top of the FX market.

Institutional FX rates come from the same place for every serious vendor: tier-1 bank contributors and the venues where the interbank market trades. Refinitiv aggregates bank contributions. Bloomberg composites bank contributions. TraderMade aggregates tier-1 bank contributions, relationships built over four decades of serving the interbank market, filtered through a quality pipeline built for programmatic consumption:

- Stale-quote suppression and outlier rejection applied upstream, before the tick reaches the client

- Crossed-market detection — a bid at or above the ask never leaves our pipeline

- Source timestamps preserved end-to-end — the tick that streams at 14:30:00.124 UTC is archived at 14:30:00.124 UTC, giving full live/history parity

The result is rate quality that stands alongside any tier-1 contributed feed and, crucially, our claim is verifiable rather than something you take on trust. Pull our tick archive for any volatile session, an FOMC release, an NFP Friday, and audit it against any reference you trust, including your current provider's feed.

And we deliver market depth. TraderMade's FX feed includes a market depth ladder on FX pairs, bid and ask levels beyond top-of-book, streamed over the same WebSocket and FIX connections. Depth-of-book is no longer something you need a venue connection or an enterprise terminal contract to access.

And the archive runs deeper than the API era. Our FX data history extends back to the 1990s as one continuous, single-source record, the same house collecting the same market through the ERM crisis, the euro's launch, the financial crisis, the SNB floor break, and every cycle since. Most API-era vendors' archives begin when their company did. Ours begins when FX started floating. For backtesting across full market regimes, not just the last bull run, that continuity is not a nice-to-have; it's the diffrence between you and your competitors.

When the rates are equivalent and depth is included, the comparison moves to everything wrapped around the data. That's where the differences become structural.

The Legacy Providers, Fairly Stated

Refinitiv / Reuters Alternatives

Refinitiv's FX franchise rests on decades of contributor relationships and one genuinely irreplaceable asset: the WM/Refinitiv benchmark rates, including the London 4pm Fix, which fund mandates and index methodologies name explicitly. If your documentation references WM/R, you buy WM/R — that's a contractual fact, not a data quality verdict.

Everything else about the relationship carries the commercial structure of the terminal era. The modernised delivery, APIs now sit alongside Elektron/RTO, but onboarding still runs through enterprise licensing, and it takes weeks, not days. The contract stacks seat licences, venue fees, and redistribution schedules into a negotiation that assumes you'll build your systems around their infrastructure. For a tier-1 bank with a market data team whose job is managing that relationship, this is business as usual. For everyone else, it's paying benchmark-provider prices for streaming rates that a modern feed delivers equivalently.

EBS

EBS is a primary interbank venue, and venue data is a different product category: the firm order book where EUR/USD, USD/JPY, and USD/CHF trade at interbank size. A systematic desk trading against the venue needs the venue's data.

But that describes a specific slice of the market. EBS coverage is strongest in its core pairs, and access follows exchange economics — venue fees, market data agreements, connectivity costs, and an onboarding process built for member firms. If you're not trading on the venue, venue data gives you one venue's view of a fragmented market. An aggregated tier-1 feed gives the broader market picture, now with depth, through a standard API integration, without venue fees or a connectivity project.

Bloomberg

Bloomberg's strength is the Terminal: a desktop workflow, a chat network, and cross-asset reference data that institutional desks organise their day around. As a human workflow tool, it has no equal.

As a machine-readable FX data source, the economics work differently. Terminal licensing is per seat, widely reported at tens of thousands of dollars per user per year, and it covers the human at the keyboard, not your application. Programmatic access means B-PIPE: a separate enterprise agreement with its own licensing scope, where application usage is negotiated and priced accordingly. That model works well for the institutions it was built for. For a platform whose product is the application, where the data needs to flow into customer-facing systems under a predictable cost structure, a per-seat and per-application model may not be best suited.

Why Product Teams Choose TraderMade as an Institutional FX Data API Alternative

The move we made in 2017, building modern API delivery on top of four decades of interbank FX heritage, is what opens the gap you see in the comparison below. The established providers have the heritage and the data quality, but that same scale makes it hard for them to move quickly. API-era startups move quickly, but without the heritage or the data standards behind them. TraderMade is rare in this comparison in holding both, and across these four dimensions the flexibility that combination offers is unparalleled.

Onboarding. Go from API key to production ticks in hours. There is no connectivity project, no infrastructure prerequisites, and no procurement gauntlet before your engineers see data. Sign up, verify your details, and the API playground is yours. Test the feed, the depth ladder, and the tick history before making any commercial commitment.

Value for money. One transparent, usage-based subscription covers streaming FX with market depth, REST, FIX, and the full tick-level historical archive. No per-seat multiplication, no separate historical contract, and redistribution terms agreed upfront rather than discovered later. On the fully-loaded, three-year TCO basis we set out in The Hidden TCO of Sub-Standard Market Data Feeds, the difference against enterprise-model providers is substantial, run your own numbers through that model and see where they land.

Flexibility. WebSocket, REST, and FIX on the same subscription, the feed fits your stack instead of your stack being rebuilt around the feed. Multi-asset on one connection: FX with depth, CFDs, crypto, indices, and equities through a single integration. Symbology, precision, and conventions are identical across live streaming, historical bars, and tick history.

Customisation. Legacy providers sell standardised products at enterprise scale; the product is the product. We build with clients, bespoke symbol sets, delivery adjustments, custom endpoints, and direct access to the engineers who run the feed. When your use case doesn't fit the standard shape, the answer is a conversation with a data engineer, not a change-request form into an enterprise queue. For platforms with specific requirements on FX data, this is the difference between a vendor and an infrastructure partner.

And underneath all four: a five-year uptime record of 99.95%, independently tracked on UptimeRobot, with zero user-impacting maintenance downtime. Reconnect gap-fill is a documented REST call against the tick archive, not a support ticket.

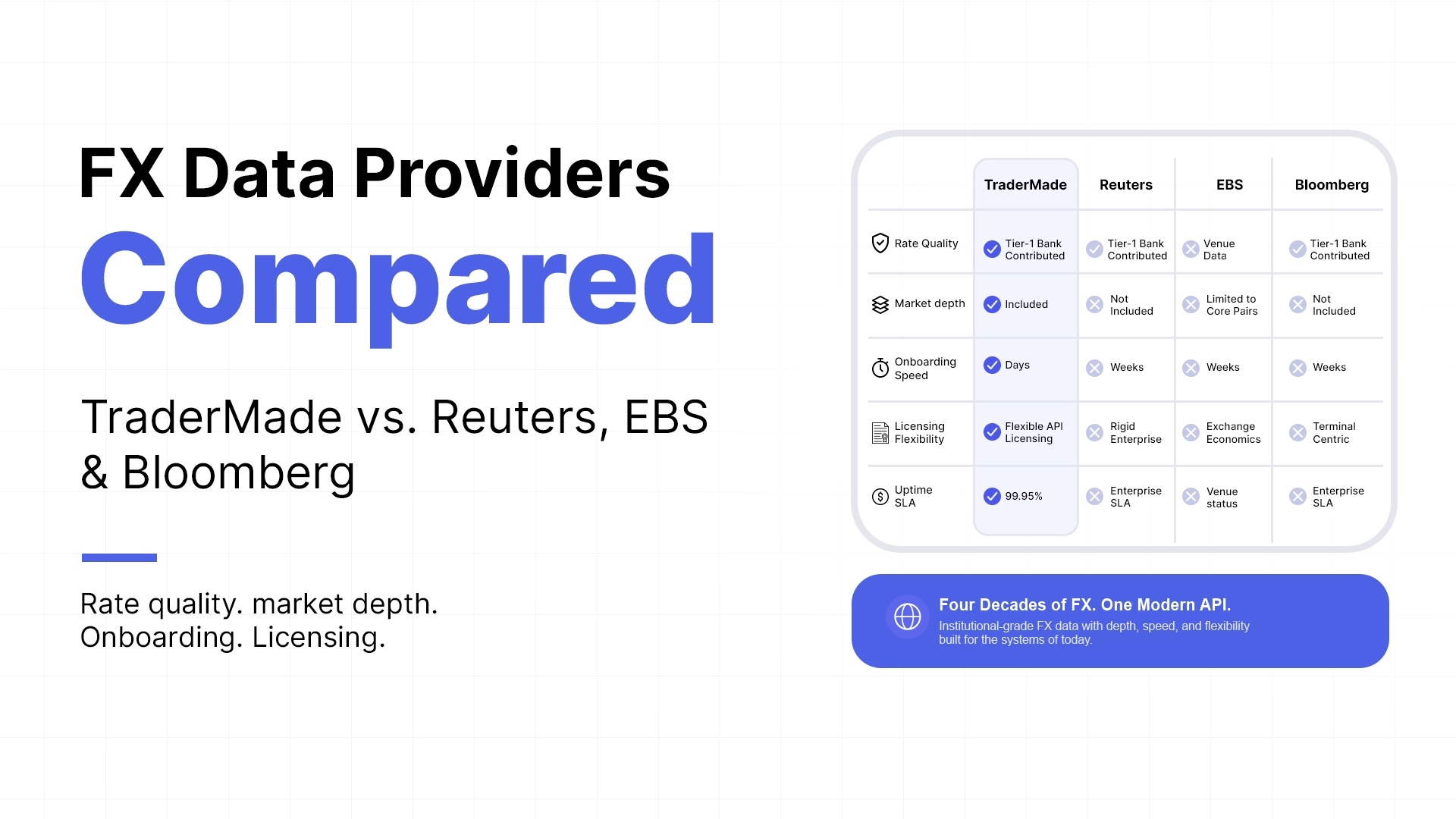

Head-to-Head

| Dimension | Refinitiv / Reuters | EBS (CME) | Bloomberg | TraderMade |

|---|---|---|---|---|

| Rate quality (FX) | Tier-1 contributed | Venue order book (core pairs) | Composite (BGN/BFIX) | Tier-1 contributed, filtered, verifiable |

| Market depth (FX) | Enterprise add-on | Venue book, core pairs only | Terminal/B-PIPE licensing | Included — ladder on FX pairs via one login flag |

| Delivery | Elektron/RTO, FIX | Venue connectivity | Terminal, B-PIPE | WebSocket, REST, FIX — one subscription |

| Onboarding | Weeks | Weeks–months | Weeks | Day or Two |

| Pricing model | Seat + venue + redistribution | Exchange fees + agreements | Per-seat + enterprise B-PIPE | Usage-based, transparent, all-in |

| Tick history & parity | Separately licensed | Venue historical products | Licensing-bound | Included, source timestamps, live/history parity |

| FX heritage | Since 1970s (Reuters Monitor) | Venue since 1990s | Terminal since 1980s | Serving interbank FX since 1984; single continuous data source from the 1990s |

| Uptime SLA | Enterprise SLA | Venue status | Enterprise SLA | 99.95% over 5 years, publicly tracked |

Information about third-party products is based on publicly available materials at the time of writing and is provided for general comparison. Product offerings, delivery options, and commercial terms change — verify current details with each vendor directly.

Where the Established Providers Remain the Right Choice

Honesty about scope makes the comparison credible, so here it is:

- You contractually need WM/R benchmark rates. Those are Refinitiv products by definition. Many of our clients keep a benchmark subscription for mandate reasons and run TraderMade as the streaming and historical backbone, the expensive mistake is letting a benchmark requirement drag the entire streaming workload onto legacy pricing.

- You trade on EBS at interbank size. Then you need the venue's own book for the venue's own market.

- Your organisation's workflow is the Terminal. Bloomberg's desktop value is real. Feeding an application, though, is a different job with different requirements, and it deserves infrastructure priced and delivered for that job.

Outside those three cases, a platform, brokerage, or quant team buying FX data in 2026 should at minimum run the comparison, the architecture and commercial model that fit a tier-1 bank's market data team are rarely the fit for a product engineering team.

Frequently Asked Questions

Is TraderMade's FX data as good as Reuters (Refinitiv)? Yes, we believe so, we both draw on tier-1 bank contributors, and TraderMade applies documented filtering (outlier rejection, crossed-market detection, cross-rate consistency) upstream. The quality is verifiable: request tick data for any volatile session and audit it yourself.

How long has TraderMade been providing FX data? Since 1984. TraderMade began as an FX charting and analysis provider to the interbank market and still provides charting services to banks today. In 2017 we expanded into API-first, data-first delivery, building on that heritage. Our FX data history extends back to the 1990s as a single continuous source.

Does TraderMade provide market depth for FX?

Yes. The WebSocket feed includes a market depth ladder on FX pairs, multiple bid and ask levels beyond top-of-book, enabled with a single send_ladder flag at login, on the same subscription.

How long does TraderMade onboarding take compared to Refinitiv or Bloomberg? Hours versus weeks. Sign up, small refundable deposit, verify your details, and an API key delivers production data the same day, no enterprise licensing negotiation before your engineers see a tick. Legacy providers have APIs now too, but access still runs through commercial negotiation and contract processes measured in weeks.

Is TraderMade a Bloomberg B-PIPE alternative? For feeding FX and multi-asset market data into applications, yes, with usage-based pricing instead of per-seat and per-application licensing. Bloomberg remains a desktop workflow tool; TraderMade is built for programmatic consumption.

Comparing FX data providers right now? Talk to a TraderMade, we'll set up a sandbox with the depth ladder enabled, hand you tick data from any event window you name, and let you run the audit against your current provider. Our scorecard works on us too.

Reuters, Refinitiv, EBS, and Bloomberg are trademarks of their respective owners. TraderMade is not affiliated with, endorsed by, or sponsored by any of these companies. References are made solely for the purpose of factual comparison.